In recent years, the European real estate market has been navigating a comprehensive yet challenging course, with ESG (Environmental, Social, and Governance) principles gaining momentum as investors prioritize sustainability decision-making. Looking beyond traditional financial metrics, they increasingly emphasize how properties contribute to a more sustainable and equitable future. While commercial real estate has been at the forefront of this shift, the residential market is emerging as a key area of focus—offering both substantial opportunities and new challenges for developers, investors, and governments alike.

This article explores the key trends reshaping the market, from evolving regulations to the role of technology in driving value—and what these changes mean for the future of European residential investment.

Key segments of the residential market

The residential market in Europe is diverse, with key segments each facing distinct challenges and opportunities:

- Social Housing: Affordable housing initiatives aimed at providing homes for lower-income individuals and families.

- Purpose-Built Student Accommodation (PBSA): Properties specifically designed for students, often located near universities and equipped with amenities tailored to student life.

- Build to Rent (BTR): Properties built specifically for long-term renting, appealing to a range of tenants, including young professionals and families.

- Care Homes: Facilities providing residential care for the elderly and those requiring assistance, reflecting growing demand in an aging population.

Each of these segments offers unique opportunities for investment and growth; however, investors must carefully navigate the shifting regulatory environment and evolving ESG standards.

Regulatory Impact and Standards

As ESG priorities intensify, the European residential real estate sector faces increasing regulatory pressure, particularly regarding energy efficiency and carbon emissions. The European Commission’s Energy Performance of Buildings Directive (EPBD) mandates that by 2030, the EU’s housing stock must achieve an energy performance certificate (EPC) rating of at least class E, with a further requirement for class D by 2033. Currently, about 25% of the EU housing stock falls below class E, while 49% is below class D. This presents a significant challenge for the housing sector, prompting investors to carefully strategize to avoid stranded assets.

In countries like France, the urgency is even more pressing. By January 2025, rental properties will be required to meet specific EPC standards, putting pressure on landlords to retrofit or divest non-compliant assets. This regulation will force the industry to rethink the entire lifecycle of residential properties, from design and construction to ongoing energy management.

Other countries, including Germany, Belgium, and the UK, are also tightening energy efficiency requirements. For instance, the Future Homes Standard in the UK, effective in 2025, mandates significant reductions in carbon emissions for new homes, pushing developers to adopt low-carbon technologies. At the same time, frameworks like GRESB (Global Real Estate Sustainability Benchmark) and CRREM (Carbon Risk Real Estate Monitor) are helping the sector measure and track ESG performance more effectively, ensuring greater accountability across the industry.

A thriving residential market, but with inherent challenges

In response to the low returns from traditional residential assets, investors are shifting towards serviced residential options like student housing, senior living, private nurseries, and co-living arrangements – all of which offer higher potential returns but come with risks related to operator reputation and financial stability.

Amid the oversupply of office space, many investors are exploring converting office buildings into residential units—a strategy that holds promise but requires expertise from asset managers to navigate the approval processes and manage capital expenditures during the transition.

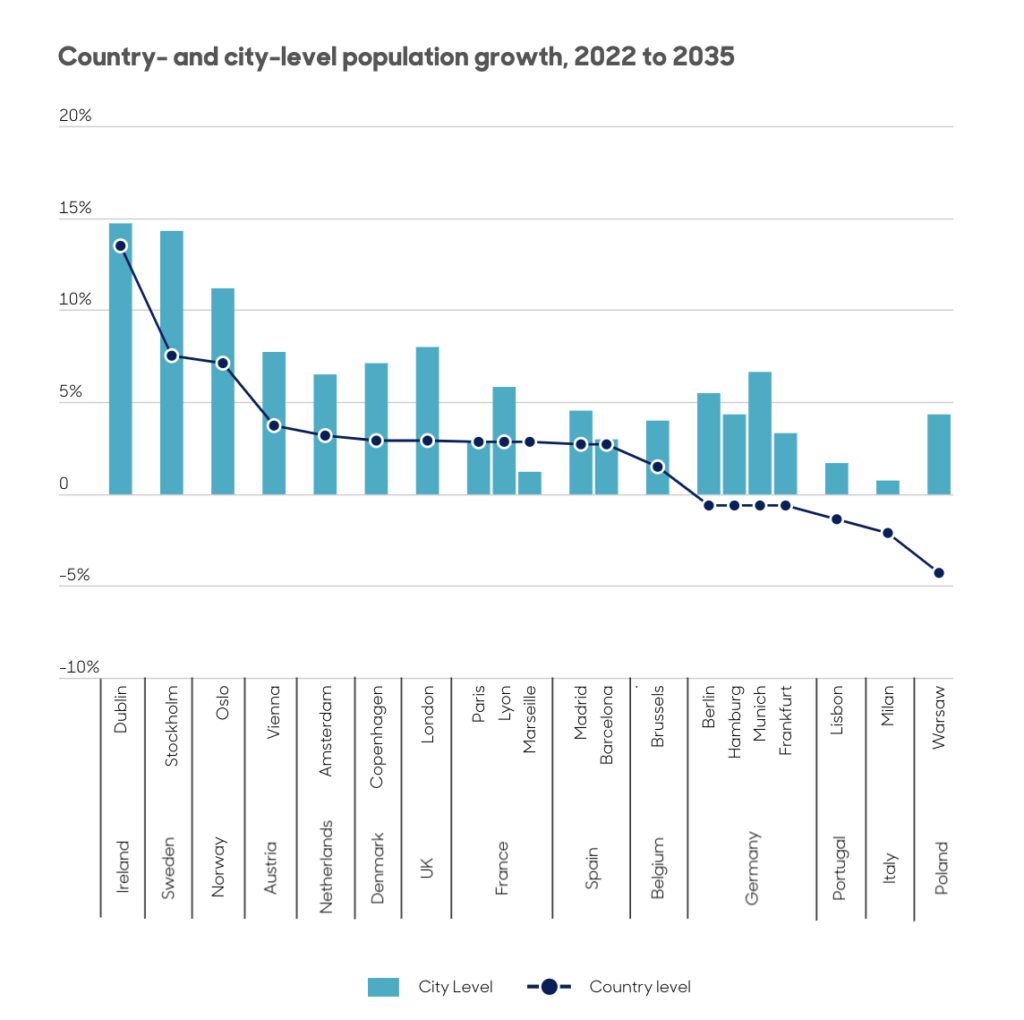

Long-term demographic trends in Europe—such as an aging population and rising demand for education—continue to underpin investor confidence in living investment strategies. Over the past decade, Europe has experienced strong population growth, increasing the need for housing. Factors like aging populations and smaller household sizes continue to shape housing demand (CBRE, 2024).

In particular, senior living is one of the most promising segments, with rising demand across countries like Germany and France, where aging populations are reaching critical mass. In Germany, more than 18.6 million people are over 65, while in France, more than one in five inhabitants is over 65 (14.7 million people).

Investment performance and the role of ESG

In recent years, investment in European residential real estate has surged, accounting for more than 20% of total real estate investment. This growth is driven by increased demand for sustainable properties and ESG-compliant assets, alongside growing interest from institutional investors and cross-border capital. These investors now see residential real estate as a stable and attractive asset class, often surpassing traditional real estate investment trusts (REITs) in activity. This shift reflects growing recognition of the sector’s long-term potential, with residential properties offering strong returns even in volatile market conditions.

In parallel, there is a growing demand for sustainable buildings and infrastructure. Investors are directing capital toward real estate companies that prioritize ESG factors, which not only align with responsible investment practices but also yield tangible financial returns. Properties that meet strict ESG criteria are becoming key differentiators in the market, often commanding higher rents. In cities like Milan, where demand for ESG-compliant buildings has spiked, property values have risen by up to 25%, underscoring the growing financial incentives tied to sustainability.

Moreover, according to index data from MSCI, pan-European residential returns have proven more resilient than commercial property, with rental cash flows mitigating some of the negative yield impacts we have seen since the market dropped in June 2022. The sector acts as a strong diversifier for institutional real estate portfolios, strongly reducing overall portfolio volatility and supporting returns. As a result, many institutions now prioritize residential strategies, with ESG-compliant assets seen as essential to sustaining long-term portfolio performance.

Quality and sustainability

The growing importance of sustainability is fundamentally transforming investment strategies in residential real estate. Banks and lenders increasingly prioritize ESG metrics, understanding that investments aligned with these principles are more likely to endure long-term. The risk of stranded assets—properties that fail to meet regulatory or ESG standards—has led to a surge in demand for energy-efficient, well-managed residential investments.

Studies from Germany and Belgium underscore the financial value of energy-efficient properties. Homes in Germany with A-rated EPC certificates can command prices up to 51% higher than those with lower ratings. In comparison, homes in Belgium with better energy efficiency fetch a 17% price premium.

Looking ahead, investors are also increasingly focusing on specific segments of the residential market, notably purpose-built student accommodation (PBSA) and the standard private rented sector (PRS). The Build-to-Rent (BTR) sector, particularly, is experiencing rapid growth, driven by young professionals and urban dwellers seeking modern, flexible living environments. Properties explicitly designed for long-term rental are becoming increasingly attractive as they cater to a lifestyle-focused demographic, offering a range of amenities tailored to convenience, comfort, and community. In 2023, the BTR market saw significant growth, and as demand for lifestyle-oriented rentals continues to rise, these developments will remain a core focus for investors.

The need for financial viability

Rising interest rates have particularly affected social housing providers reliant on public funding. This highlights the need to balance financial viability with sustainability goals. As the sector faces growing regulatory pressure, maintaining profitability while meeting ESG compliance is becoming an ever-greater challenge.

Deepki’s platform serves as a single source of truth, providing visibility at the asset level across Europe. This allows operators to track and manage ESG investments effectively, ensuring compliance with evolving regulations while recovering the associated costs. Deepki enables operators to streamline their decision-making processes and maximize long-term value by using data-driven insights.

What is in store for Europe’s residential market?

The pressing question for existing and future strategies for residential investing is how best to adapt to the changing dynamics in the market. As we have learned from the commercial real estate markets, retail or office over the last decade, standing still and failing to adapt can expose you to obsolescence regarding assets and investment strategy.

For those operating in the residential market, the next few years will be a defining period. The key to success lies in adapting to new regulations and embracing innovative technologies. As the 2025 Future Homes Standard approaches, the ability to stay ahead of regulatory changes and capitalize on emerging opportunities will be critical for long-term success.

At Deepki, we are committed to helping residential operators navigate these challenges. Our pan-European expertise and ESG-focused solutions provide the tools needed to ensure compliance, drive performance, and maximize long-term value in the rapidly changing landscape of residential real estate.

WHITE PAPER

Real estate’s ESG imperative: from challenge to opportunity

Download Deepki’s white paper to learn more about the current state of ESG in the real estate sector. It will help anticipate your next move by acknowledging the key trends to watch. Additionally, it will help understand how decisive action when embracing transparency, collaboration, and engagement throughout the value chain can go a long way.