Over the last ten years, the issue of “stranded assets” resulting from diverse types of risk factors has loomed larger in the real estate industry. The 2015 Paris Agreement brings all nations into a common cause to undertake ambitious efforts to reduce the challenge of climate change and adapt to its effects. The collective goal is to ‘decrease the global average temperature to well below 2 °C above pre-industrial levels as well as to limit the temperature increase to 1.5 °C above pre-industrial levels.’

Therefore, a greater number of cities and countries are starting to make the necessary changes to meet expected legislative requirements in order to achieve net zero emissions by 2050. As a more concrete example, the Paris Agreement implies a reduction in CO2 emissions for the real estate sector of 77% by that date. To abide by this landscape, building owners are facing increasing pressure to be more transparent and to implement changes to not fall behind. As the real estate industry is responsible for approximately 39% of energy-related CO₂ emissions globally, making it a key target in global efforts to reduce carbon emissions, a better knowledge of the risks related to climate change is starting to develop. Regarding long term investments, stranding risks require increased attention.

What are stranded assets?

A stranded asset is an investment that loses its value prior to the end of its anticipated useful and economic life because of the impact of various changes. It is defined as an asset that has suffered from unanticipated or premature devaluation. While the topic is not new in the real estate sector, the influence and systemic reach of climate change and associated environmental policy on some property assets and related capital markets exposes assets to a greater amount of risks. Among these are the environment-related ones that can cause asset stranding such as environmental challenges, new government regulations or even evolving social norms.

First, climate change influences weather patterns around the world, projections indicate an increase in the frequency and intensity of extreme events: floods, forest fires, land movements, etc. This long-term change also exposes assets to another threat: that of becoming “stranded” due to their incompatibility with a low-carbon economy as sustainability regulations, such as SFDR or the European Taxonomy, and market become stricter.

Read more: Understanding the EU Green Taxonomy in 7 questions

Factors that cause stranded assets also include falling clean technology costs (e.g. solar photovoltaic) and changes in consumer behavior asking for better environmental performance (e.g. certification schemes). Indeed, there is a clear and increased demand for green buildings, both in transactions among investors and on the tenant market. More stakeholders realize that aligning to an effective ESG strategy is not just about safeguarding our future and ecosystems, it is also the value of real estates and investments.

Read more on Green Premium and Brown Discounting: the impact of ESG performance on asset value

How can this scenario impact your portfolio?

Investors and Asset Managers are increasingly being asked to implement an investment strategy that supports the transition to a low-carbon economy and is resilient to climate risks. In recent years, the problem of stranded assets caused by environmental factors has become increasingly more present. Indeed, buildings with particularly high CO2 emissions will lose so much value that it will no longer be possible to sell them on the commercial real estate market, thus turning them into stranded assets.

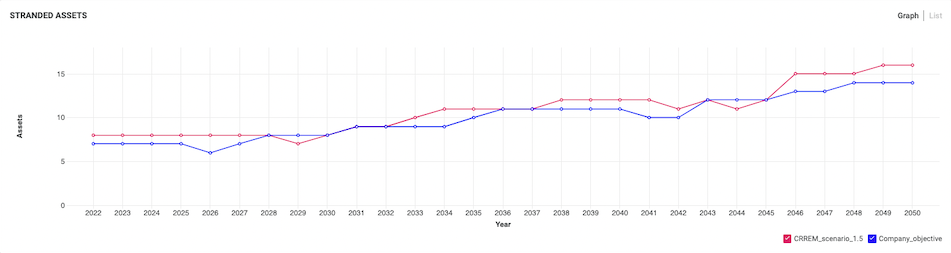

Therefore, in this context, stranded assets are properties that will not meet future energy efficiency standards and market expectations and might be increasingly exposed to the risk of early economic obsolescence in the near future. Tools such as the CRREM (Carbon Risk Real Estate Monitor) have been developed to guide real estate actors towards a trajectory compatible with European objectives. But if GHG reduction and energy consumption targets are not met by the defined dates, the EU and national authorities will certainly tighten their policies, increasing the financial risk for investors who do not participate.

Managing assets exposed to this risk

New net zero carbon buildings are important in helping achieve the EU’s sustainability target but improving existing buildings — which make up the majority of the current building sector — should be the primary focus. Indeed, around 80% of the buildings built today will still be standing in 2050.

Read more: Retrofitting: 5 reasons why you shouldn’t overlook it

Asset Managers are liable for the impact of their assets in the shift to a cleaner, more virtuous economy. Currently Asset Managers and owners can take various initiatives to reduce the current GHG emissions and energy consumption of each of their assets or even their entire portfolio. In order to take action to assure the future of their assets, they need to have a better understanding of risks and opportunities among their holdings. Deepki’s data intelligence platform allows users to project and visualize pathways to predict their future ESG performance and thereby allocate their resources to the most efficient course of action.

Read more: What is resilience ?

Trajectories allow investors to anticipate the consequences of GHG intensity reduction targets on specific assets and their portfolio.

To achieve consistent long-term performance and sustainability goals, the understanding of the consequences of stranded assets is key. Despite the tough call on these actors, who are already hard-pressed for time, the rewards for getting on top of this are worth the effort. By understanding the different risks to which assets are exposed, asset managers and investors can build a complete picture that allows them to best position themselves to improve their green portfolio and profit from it.